How to Get Short-Term Health Insurance?

Key Takeaways

- Short-term health insurance can help cover temporary gaps, such as between jobs or during a waiting period before employer benefits begin.

- These plans are not ACA-compliant, which means pre-existing conditions and certain essential health benefits may not be covered.

- While premiums are often lower than traditional plans, deductibles, exclusions, and out-of-pocket maximum expenses may be significantly higher.

Key Takeaways:

You can get short-term health insurance directly from private insurers to cover temporary gaps between jobs or waiting periods. These plans start quickly but are not ACA-compliant, so pre-existing conditions and some essential benefits may not be covered. This guide explains how temporary health insurance works and how to choose the right plan safely.

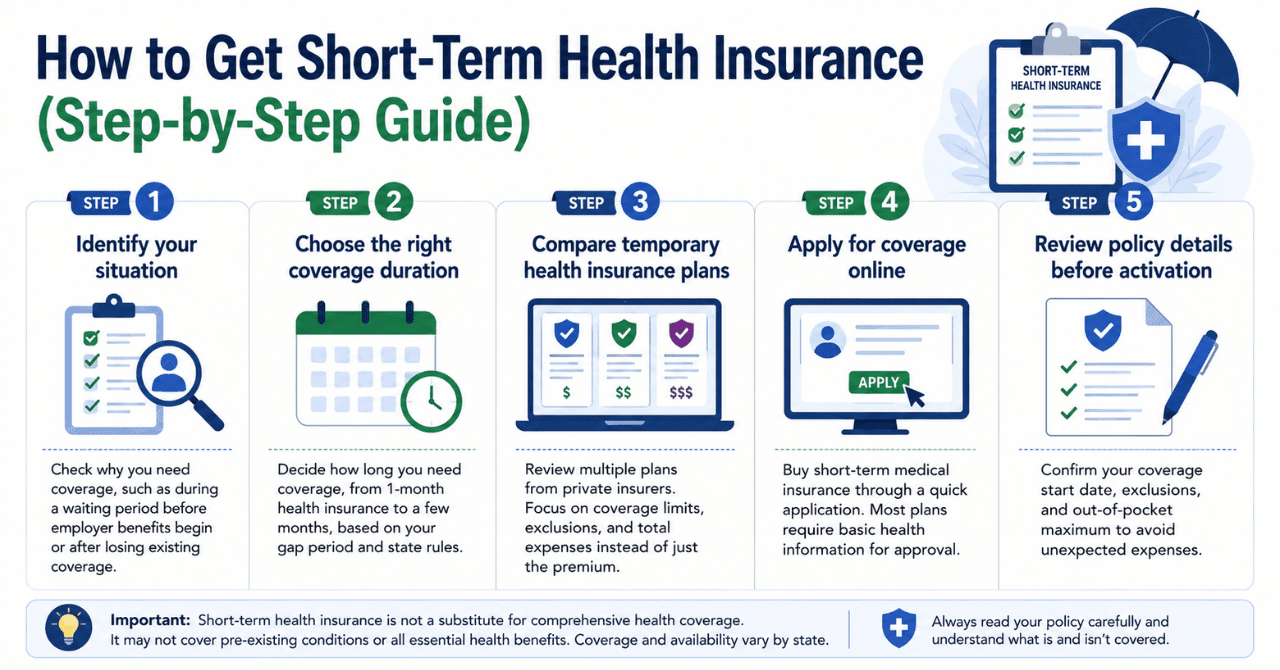

How to Get Short-Term Health Insurance (Step-by-Step Guide)

You can get this temporary health insurance by following a clear, action-based process that helps you choose the right plan quickly and safely.

Step 1: Identify your situation

- Check why you need coverage, such as during a waiting period before employer benefits begin or after losing existing coverage

Step 2: Choose the right coverage duration

- Decide how long you need coverage, from 1-month health insurance to a few months, based on your gap period and state rules.

Step 3: Compare temporary health insurance plans

- Review multiple plans from private insurers. Focus on coverage limits, exclusions, and total expenses instead of just the premium.

Step 4: Apply for coverage online

- Buy short-term medical insurance through a quick application. Most plans require basic health information for approval.

Step 5: Review policy details before activation

- Confirm your coverage start date, exclusions, and out-of-pocket maximum to avoid unexpected expenses.

According to the Centers for Medicare & Medicaid Services (CMS), you can purchase health insurance directly from private companies or through agents, which supports how short-term plans are typically obtained outside government programs.

Where to Get Short-Term Health Insurance Plans Quickly

Temporary health insurance is available directly from private insurers or licensed agents, as these plans are sold outside government programs. They are not available through the ACA Marketplace because they are not ACA-compliant, which is why you need to apply separately for this type of coverage.

If you recently lost employer coverage, you may also consider COBRA insurance, which allows you to continue your current plan for a limited time. The USAGov states that you typically have up to 60 days to elect COBRA coverage after a qualifying event, giving you time to choose between continuing your current plan or switching to a short-term option.

Who Should Get Short-Term Health Insurance

Short-term policies work best for healthy individuals who need temporary gap coverage before getting permanent insurance.

- People between jobs: Temporary health insurance between jobs can help you stay covered until your new employer plan begins.

- People waiting for employer benefits: If your workplace has a waiting period before benefits start, short-term coverage can fill that gap.

- People who missed the open enrollment period: If you do not qualify for a special enrollment period, short-term plans may provide temporary protection outside ACA enrollment windows.

- Young adults losing dependent status: Young adults can stay on a parent’s ACA plan until age 26. After that, short-term coverage may help until you secure a long-term option.

What Short-Term Health Insurance Covers And Does Not Cover

Temporary health insurance mainly provides emergency-style protection instead of full health coverage. Because these plans do not have to meet ACA compliance standards, they usually offer fewer benefits than traditional health insurance plans.

| Generally Covered | Commonly Excluded |

|---|---|

| Emergency room visits | Pre-existing conditions |

| Doctor visits | Maternity care |

| Urgent care services | Mental health treatment |

| Hospitalization for sudden illness or injury | Preventive care |

| Limited prescription coverage (varies by plan) | Comprehensive prescription benefits |

← Swipe to see more →

Pros and Cons of Short-Term Health Insurance

If you are debating whether this temporary coverage is right for you, here is a direct breakdown of the benefits versus the financial risks.

| Pros | Cons |

|---|---|

| Helps cover temporary gaps in insurance | Pre-existing conditions are usually not covered |

| Coverage can start quickly, sometimes within 24 hours | Deductibles and out-of-pocket maximum expenses may be higher |

| Plans can often be canceled without penalties | Benefits and coverage vary significantly between plans |

| Lower monthly premiums than many ACA plans | Mental health, maternity, and preventive care may be excluded |

| Useful during waiting periods or between jobs | Medical underwriting may be required for approval |

← Swipe to see more →

How Long Can You Have Short-Term Health Insurance

Federal rules generally restrict these plans to an initial term of less than 3 months, with total coverage lasting no more than 4 months, including renewals. State laws also affect how long you can stay covered.

Some states apply stricter limits or do not allow temporary health insurance plans at all, while others permit longer coverage periods. Renewal is also not guaranteed, especially if your health status changes during the coverage period.

The Bottom Line: Is It Safe to Get Short-Term Health Insurance?

Short-term health insurance can help during temporary coverage gaps, but it is not a long-term replacement for comprehensive insurance. These plans do not follow ACA protections and may limit coverage for pre-existing conditions and essential health benefits. These plans may help if you are between jobs or waiting for employer benefits to begin. However, a permanent ACA-compliant health plan remains the safer long-term option.

Frequently Asked Questions

Yes, you can usually buy short-term medical insurance throughout the year because these plans are not tied to the ACA open enrollment period.

No, most short-term health insurance plans do not cover pre-existing conditions and may deny claims related to existing medical issues.

Short-term plans may exclude maternity care, mental health treatment, preventive services, and comprehensive prescription coverage. They also may have higher deductibles and limited benefits compared to ACA plans.

Medical Disclaimer

This blog is provided for informational purposes only and does not replace professional medical, insurance, or financial guidance. The content is based on publicly available resources from trusted organizations, including the Centers for Medicare & Medicaid Services (CMS), USAGov, and MedlinePlus. Coverage rules, eligibility, and state regulations may change over time and vary by provider. Always consult a licensed insurance representative, healthcare professional, or official government resource before making coverage decisions.