How to Read Summary of Benefits and Coverage for GLP-1: 2026 Guide Decoded

Key Takeaways

1. An SBC gives a broad view of prescription benefits, costs, limits, and exceptions.

2. Exact GLP-1 coverage usually needs the plan's formulary or drug list.

3. Check the GLP-1 drug name, tier, prior authorization, and step therapy rules.

4. Coverage gaps may include exclusions, quantity limits, or high cost-sharing.

5. If gaps appear, confirm details with your insurer and pharmacy benefits team.

6. Compare verified coverage, appeal, assistance, and licensed pharmacy options carefully.

A Summary of Benefits and Coverage can reveal important details about GLP-1 access. This patient guide GLP-1 coverage explains how to read Summary of Benefits and Coverage for GLP-1 in 2026. It shows where prescription benefits appear and what coverage terms mean. You can use it to spot costs, restrictions, and gaps before filling a prescription.

What Is a Summary of Benefits and Coverage for GLP-1 Drugs?

A Summary of Benefits and Coverage is a short plan document. It explains major benefits, cost-sharing rules, limits, and exceptions. This SBC explanation GLP-1 benefits section helps clarify prescription benefit basics. However, an SBC usually does not confirm every drug-level rule. You still need the plan formulary for exact GLP-1 coverage details. The formulary may show tier placement, prior authorization, and step therapy. Use the SBC as the first checkpoint, not the final answer.

Where to Find GLP-1 Coverage Details in a Summary of Benefits and Coverage

Start with the prescription drug section of your Summary of Benefits and Coverage. It may show general drug benefits, tiers, and cost-sharing rules. Then look for links to the formulary, pharmacy benefits summary, or insurer portal. Exact GLP-1 details are usually outside the SBC. These documents help confirm drug-level coverage rules.

How to Check If GLP-1 Drugs Are Covered in Your SBC

Your SBC can show whether prescription drug benefits are included. For exact GLP-1 coverage, use the formulary or drug list. Search by the exact drug name, not only the drug class. GLP-1 receptor agonists may include semaglutide or tirzepatide products.

- Start with the prescription drug section in your SBC.

- Open the plan formulary linked in your insurer portal.

- Search for the exact GLP-1 drug name.

- Check whether the drug is covered, restricted, or excluded.

- Review the drug tier and expected cost-sharing.

- Look for prior authorization, step therapy, or quantity limits.

- Call the pharmacy benefits number if anything is unclear.

What Prior Authorization Means for GLP-1 Coverage in an SBC

Prior authorization means your plan may require approval before covering a GLP-1 drug. The SBC may mention this rule under prescription drug benefits. However, the formulary usually gives the exact drug-level requirement. Look for labels such as “PA,” “authorization required,” or “approval needed.”

If prior authorization applies, coverage is not automatic. Your prescriber may need to submit supporting documentation. The insurer may review the diagnosis, plan criteria, and prescription details before making a decision. Patients should confirm prior authorization requirements with the pharmacy benefits number. Approval rules can vary by plan, drug, and coverage reason.

What Step Therapy Means for GLP-1 Coverage in an SBC

Step therapy means a plan may require another covered drug first. For GLP-1 coverage, this rule may appear in the formulary notes. The SBC may only point you toward prescription drug rules. Look for labels such as “ST,” “step therapy,” or “trial required.”

If step therapy applies, the first requested GLP-1 may not be covered immediately. Your prescriber may need to show previous medication history. They may also request an exception if plan rules allow it. Always confirm step therapy protocols with the insurer’s pharmacy benefits team.

How to Read GLP-1 Costs in a Summary of Benefits and Coverage

GLP-1 coverage can still be costly, even when a plan includes prescription benefits. The SBC may show cost-sharing rules, but not always drug-specific prices. Use these terms to understand what you may pay before checking the formulary or insurer portal.

| SBC Cost Term | What It Means for GLP-1 Coverage |

|---|---|

| Deductible | Amount you may pay before plan benefits begin. |

| Copay | Fixed amount for a covered prescription. |

| Coinsurance | The percentage of the covered drug cost you may pay. |

| Drug tier | A category that may affect your prescription cost. |

| Out-of-pocket maximum | Yearly limit for covered in-network costs. |

| In-network pharmacy | A pharmacy that may offer lower covered costs. |

| Non-preferred drug | Drug that may have higher cost-sharing. |

← Swipe to see more →

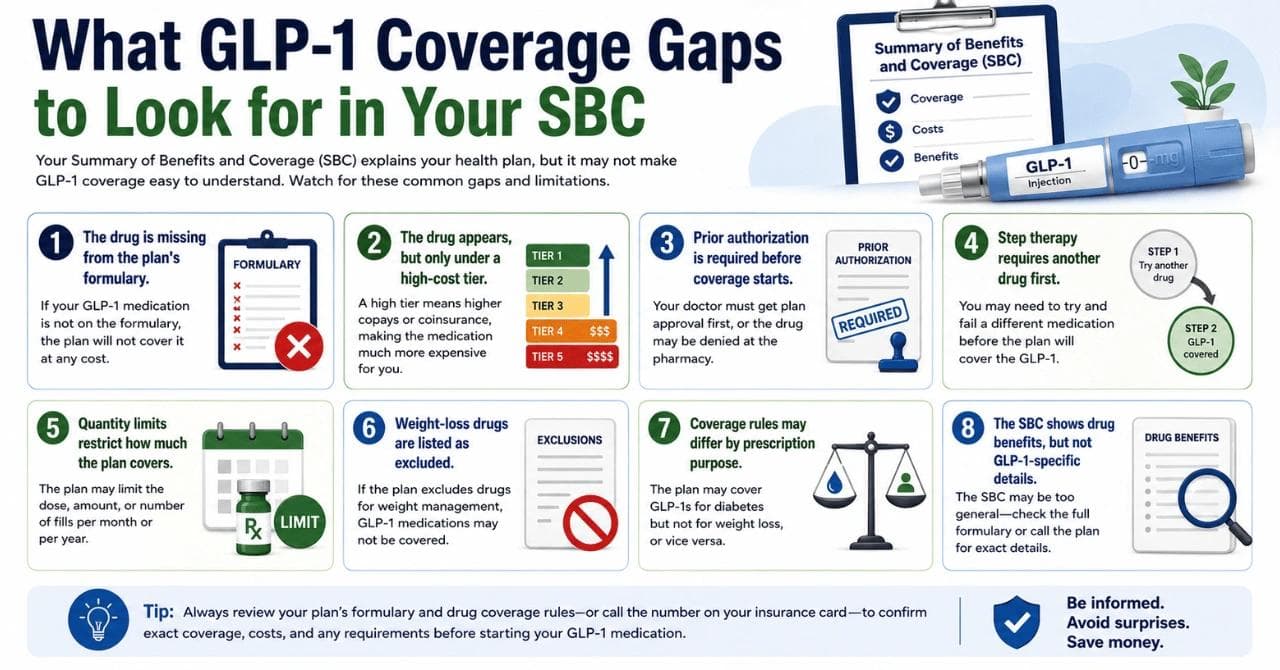

What GLP-1 Coverage Gaps to Look for in Your SBC

Coverage gaps can appear even when your SBC shows prescription drug benefits. A GLP-1 may still have restrictions, higher cost-sharing, or limited coverage. Review the SBC, formulary, and pharmacy benefit notes together.

Look for these possible GLP-1 coverage gaps:

- The drug is missing from the plan's formulary.

- The drug appears, but only under a high-cost tier.

- Prior authorization is required before coverage starts.

- Step therapy requires another drug first.

- Quantity limits restrict how much the plan covers.

- Weight-loss drugs are listed as excluded.

- Coverage rules may differ by prescription purpose.

- The SBC shows drug benefits, but not GLP-1-specific details.

These gaps do not always mean coverage is impossible. They show what needs to be confirmed before filling the prescription.

What to Do If Your Summary of Benefits and Coverage Shows GLP-1 Gaps

If your SBC shows GLP-1 coverage gaps, start by confirming the details. Call the insurer’s pharmacy benefits number and ask about the exact drug. Check whether the issue is formulary status, prior authorization, step therapy, quantity limits, or exclusion.

Next, ask your prescriber what documentation may support coverage. If the plan denies coverage, review the appeal or exception process in your plan documents. You can also ask the insurer how to submit forms, records, or a coverage review request.

You can compare other legitimate paths as well. These may include manufacturer support programs, enrollment-period plan changes, patient assistance resources, or licensed pharmacy choices. If coverage gaps remain, some patients review Canadian pharmacy pricing for comparison. Polar Bear Meds can help patients review available pharmacy pricing, prescription requirements, and ordering details.

Bottom Line on Summary of Benefits and Coverage for GLP-1

A Summary of Benefits and Coverage is a useful starting point for GLP-1 coverage. It can show prescription benefit basics, cost-sharing rules, and plan limits. However, the formulary gives a clearer drug-level answer. Always check tier status, prior authorization, step therapy, and exclusions before filling a prescription. If any gaps remain, carefully compare all verified coverage and pharmacy options.

Frequently Asked Questions

Not always. An SBC may show general copay, coinsurance, and deductible rules. The exact GLP-1 cost usually requires checking the formulary, insurer portal, or pharmacy benefits team.

Some plans apply different rules based on the prescription purpose. A drug may be reviewed differently for diabetes, weight management, or another approved use. Always confirm the coverage reason with your insurer.

Yes. Your prescriber may submit documentation if prior authorization is required. This may include diagnosis details, prescription information, and plan-requested records. The insurer makes the final coverage decision.

Ask whether the exact GLP-1 is on your formulary. Also ask about tier, copay, coinsurance, prior authorization, step therapy, quantity limits, and exclusions. Request written confirmation when possible.

Disclaimer

This blog is for general information and insurance-navigation purposes only. It is not medical, legal, pharmacy, or insurance advice. GLP-1 coverage, formulary status, prior authorization, step therapy, costs, and exclusions can change. Rules may vary by plan, employer, insurer, state, diagnosis, and prescription purpose. Always confirm details with your insurer, prescriber, pharmacy benefits team, and official plan documents before making coverage or purchase decisions.