Affordable GLP-1 Access for Freelancers: A 2026 Cost Savings Guide

Key Takeaways

1. Brand-name GLP-1 costs can be high without coverage, so savings cards and patient assistance programs should be checked first.

2. Compounded GLP-1 options are not FDA-approved, and the FDA has warned about safety and dosing concerns.

3. Medicare’s GLP-1 Bridge starts July 1, 2026, with a $50 monthly copay for eligible Part D beneficiaries.

4. HSA/FSA eligibility depends on whether the medication is tied to a diagnosed medical condition and plan rules.

Affordable GLP-1 medications are harder to reach than ever for people without employer-sponsored insurance. Brand-name GLP-1 medications can cost hundreds to more than $1,000 per month without coverage, depending on the drug, dose, pharmacy, insurance status, and savings program. This guide breaks down every realistic path to GLP-1 cost savings in 2026, including specific programs, dollar amounts, and steps you can take today.

GLP-1 Costs Hit Freelancers Hard in 2026

GLP-1 agonists have grown quickly in the U.S., and more patients are now comparing insurance, savings programs, and cash-pay options before filling prescriptions. That's a massive patient population, and a growing share of them are struggling to pay. Without insurance, many brand-name GLP-1 medications can cost hundreds to more than $1,000 per month, depending on the drug, dose, pharmacy, and savings program.

For freelancers, the problem is compounded. You're not getting a subsidized employer plan. Your freelance income GLP-1 budget can change month to month, making predictable medication costs harder to manage. And in 2026, many insurers are actively limiting or dropping GLP-1 coverage for weight loss, adding prior authorization requirements and step therapy protocols that can delay access by weeks or months.

Even when coverage technically exists, it often requires proving a specific BMI, documented comorbidities, and evidence of prior lifestyle interventions before a claim gets approved. That's a lot of paperwork for someone running a solo business.

The drug prices aren't going to drop overnight. But there are real, concrete strategies to reduce what you're paying.

Manufacturer Savings Cards and Patient Assistance: Your First Move Toward GLP-1 Cost Savings

Start here. GLP-1 coupon programs, savings cards, and pharmaceutical programs can reduce prescription savings gaps if you qualify.

Novo Nordisk offers savings cards for both Wegovy and Ozempic, which can help with Wegovy access and Ozempic affordability for eligible patients. Novo Nordisk and Eli Lilly offer savings programs for eligible commercially insured patients. Some official savings offers advertise costs as low as $25, but eligibility rules, maximum savings, coverage status, and government-insurance exclusions apply. These Wegovy discount programs and tirzepatide savings offers are worth checking before anything else.

If you're uninsured or have a low income, patient assistance programs are the next step. Both Novo Nordisk and Eli Lilly run PAPs that provide free or deeply discounted medication to eligible individuals who can demonstrate financial need. You'll need documentation, but for people who qualify, these programs can eliminate the cost entirely.

Cash-Pay Options: Canadian Pharmacies and Compounded GLP-1 Caution

Some freelancers compare cash-pay options when brand-name GLP-1 medications are unaffordable or not covered, especially when looking for semaglutide cost reduction routes. This may include licensed Canadian pharmacies, local pharmacy discount tools, manufacturer direct-pay programs, or compounded GLP-1 options.

A licensed Canadian pharmacy can be useful as a price-comparison reference for U.S. patients paying out of pocket. Polar Bear Meds, for example, lists Canadian pharmacy pricing for prescription medications and requires a valid prescription before dispensing. This makes it one option to compare against U.S. cash prices, savings cards, and insurance copays.

However, this route should not replace medical or legal guidance. U.S. patients should confirm the medication, dose, prescription status, pharmacy licensing, shipping timeline, and total cost before ordering. They should also understand that FDA personal importation rules are strict, and importing prescription drugs into the U.S. may not be permitted in many situations.

Compounded GLP-1 products need extra caution. Compounded drugs are not FDA-approved, and the FDA has warned about safety, quality, and dosing concerns with unapproved GLP-1 products. Review this option only through a licensed telehealth or in-person prescriber and a properly licensed compounding pharmacy.

Medicare GLP-1 Bridge Program (July 2026–December 2027)

If you're on Medicare, there's meaningful new relief starting July 1, 2026. The Medicare GLP-1 Bridge program, as outlined on medicare.gov, provides eligible beneficiaries with select GLP-1 medications at a fixed $50 monthly copay. The program runs through December 31, 2027.

Participating manufacturers have agreed to provide these medications at a reduced net cost of approximately $245 per month, according to CMS data. The $50 copay structure means that Medicare patients pay a fraction of that amount. This is a temporary demonstration program, not a permanent benefit, so the coverage window matters. Check CMS.gov for the full list of covered drugs and specific eligibility requirements, as not all GLP-1 medications are included.

HSA and FSA: Tax-Advantaged Paths to Affordable GLP-1s

Using a health savings account or flexible spending account is one of the most underused strategies for reducing prescription costs. Some GLP-1-related costs may be HSA/FSA eligible when tied to a physician-diagnosed condition, such as obesity or diabetes. Confirm eligibility with your HSA/FSA custodian before paying. Paying through these accounts means you're using pre-tax dollars, which lowers your effective cost based on your marginal tax rate.

For freelancers with variable income, the HSA has a particular advantage. Unlike an FSA, your contributions roll over year to year, and you control the timing. In a high-income month, you can contribute more; in a lean month, you draw from the balance. Request a Letter of Medical Necessity from your prescribing provider upfront. Some account custodians require this documentation for GLP-1 purchases, and having it ready avoids delays at the pharmacy.

Medication coupons and savings tools can also be stacked with HSA/FSA payments in some cases, so check whether your specific savings card allows that combination.

Insurance Reality Check: Coverage Gaps and Appeal Strategies for GLP-1 Insurance Coverage

The insurance picture in 2026 is genuinely uneven. Medicaid coverage for GLP-1 medications varies by state and by diagnosis. Some state Medicaid programs may cover GLP-1 drugs for diabetes management, while weight-loss coverage can be more limited. Check your state Medicaid formulary or benefits office before assuming coverage. If you're on Medicaid and live in one of those four states, you're effectively on your own for weight loss indications.

Private insurance is more promising but still inconsistent. Approximately 45% of large employers now include at least one anti-obesity medication on their formulary, up from roughly 25% in 2023, according to data from the American Association of Obesity and Preventive Medicine. But "on the formulary" doesn't mean easy to access. Prior authorization requirements are nearly universal, and step therapy protocols, where insurers require you to try cheaper alternatives first, are increasingly common.

If you're denied, appeal. Document your BMI, any relevant comorbidities, and your history of lifestyle modification attempts. Your doctor's office can often submit supporting clinical notes that strengthen an appeal significantly. Work with your prescriber's team rather than navigating the process alone.

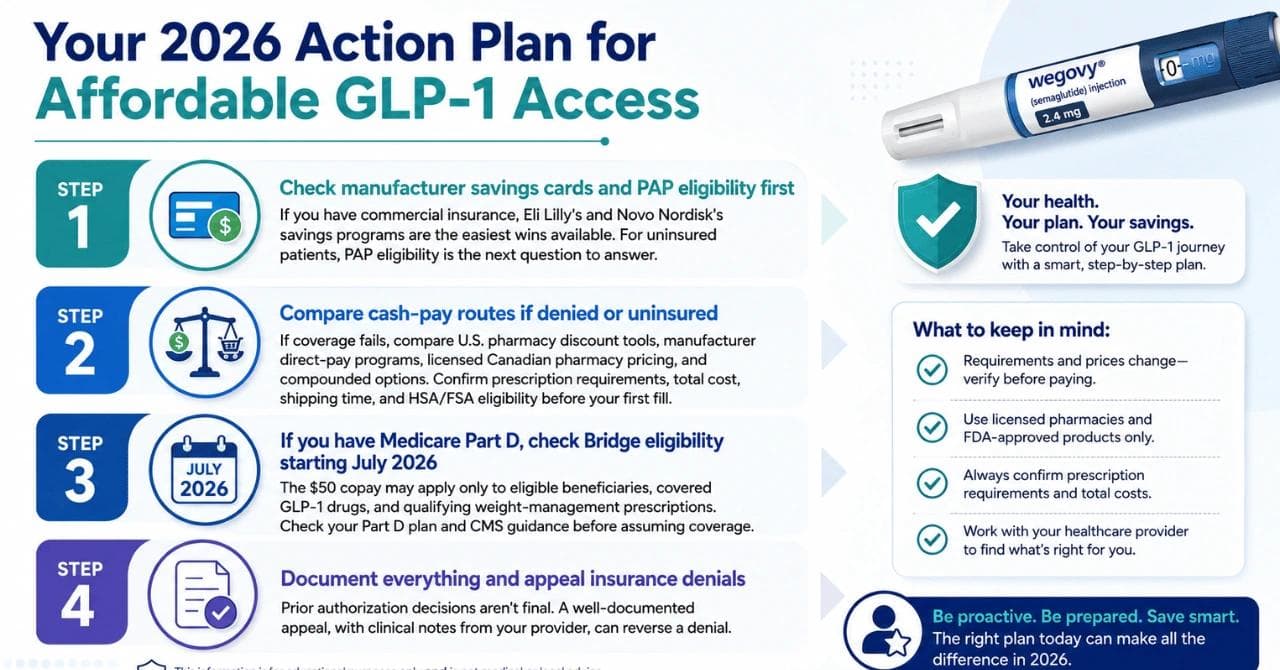

Your 2026 Action Plan for Affordable GLP-1 Access

Getting to an affordable GLP-1 regimen as a freelancer requires working through options in a logical order. Here's how to approach it.

Step 1: Check manufacturer savings cards and PAP eligibility first

If you have commercial insurance, Eli Lilly's and Novo Nordisk's savings programs are the easiest wins available. For uninsured patients, PAP eligibility is the next question to answer.

Step 2: Compare cash-pay routes if denied or uninsured

If coverage fails, compare U.S. pharmacy discount tools, manufacturer direct-pay programs, licensed Canadian pharmacy pricing, and compounded options. Confirm prescription requirements, total cost, shipping time, and HSA/FSA eligibility before your first fill.

Step 3: If you have Medicare Part D, check Bridge eligibility starting July 2026

The $50 copay may apply only to eligible beneficiaries, covered GLP-1 drugs, and qualifying weight-management prescriptions. Check your Part D plan and CMS guidance before assuming coverage.

Step 4: Document everything and appeal insurance denials

Prior authorization decisions aren't final. A well-documented appeal, with clinical notes from your provider, can reverse a denial.

GLP-1 cost savings don't happen by accident. They come from knowing which programs exist, qualifying for the right ones, and pushing back when coverage is wrongly denied. As a freelancer, you don't have an HR department handling this for you, so the legwork falls on you. Start with the easiest options first, and work down the list.

You can also read more articles on medication costs and savings strategies to stay current as insurance policies continue to shift throughout 2026.

Bottom Line: Affordable GLP-1 Access Starts With the Right Order

Affordable GLP-1 access in 2026 is not about choosing one shortcut. It is about checking each option in the right order. Start with manufacturer savings cards and patient assistance programs. Then compare insurance appeals, HSA/FSA payment options, Medicare support, and safe cash-pay alternatives.

Freelancers do not have an HR team managing coverage changes for them. That makes documentation, medication costs, drug prices, and regular eligibility checks even more important. The best strategy is simple: start with the lowest-cost qualified option, keep proof for every expense, and review your plan whenever insurance rules change.

Frequently Asked Questions

Manufacturer savings cards from Novo Nordisk and Eli Lilly are the fastest starting point, potentially bringing monthly costs to $25 for commercially insured patients. If you're uninsured, compounded GLP-1 options through telehealth platforms run $79-$350 per month, and patient assistance programs can provide medication at no cost for those who qualify. Paying through an HSA or FSA with pre-tax dollars, or using a prescription discount tool like GoodRx to compare cash prices at local pharmacies, can reduce out-of-pocket costs further.

Patient assistance programs are run by pharmaceutical companies like Novo Nordisk and Eli Lilly to provide free or deeply discounted medication to uninsured or low-income patients who meet specific eligibility criteria. These differ from manufacturer savings cards, which are designed for commercially insured patients. Medicare patients are excluded from manufacturer card programs, but the new Medicare GLP-1 Bridge program starting July 1, 2026 offers a government-backed alternative with a $50 monthly copay through December 2027.

Coverage varies sharply depending on your plan and state. Many private insurers are limiting or dropping weight-loss GLP-1 coverage in 2026, typically requiring prior authorization and step therapy before approving claims. Medicare now offers temporary coverage through the Bridge program at a $50 monthly copay, running through December 2027. Medicaid coverage depends on your state, with only 13 states covering GLP-1s for obesity as of January 2026 and four states having removed coverage entirely.

Disclaimer

This article covers what the research shows about GLP-1 costs and savings programs, but it's not medical or financial advice. Drug pricing, insurance policies, and program eligibility change frequently. Before starting any GLP-1 medication or making changes to your treatment, talk to your doctor or a licensed pharmacist who knows your full health picture.