How to Negotiate GLP-1 Coverage Back Into Your Employer's 2026 Plan

Key Takeaways

1. GLP-1 coverage may depend on employer plan design, diagnosis, and formulary rules.

2. Employees should check the 2026 SBC, formulary, and prior authorization details.

3. A strong HR request should include documents, denial details, and prescriber support.

4. Cost-benefit points should focus on access, affordability, and employee needs.

5. If coverage is delayed, compare appeals, marketplace plans, and pharmacy pricing options.

Losing GLP-1 coverage can feel frustrating, especially before a new plan year. To learn how to negotiate GLP-1 coverage back, start with clear documents and a calm HR request. Your doctor’s support and denial details can help frame the issue clearly. Cost concerns can guide employer health plan GLP-1 negotiation.

Why GLP-1 Coverage May Be Missing From Your Employer's 2026 Plan

GLP-1 coverage may be missing because employer plans manage pharmacy spending carefully. Some plans cover GLP-1 receptor agonists for diabetes management. Others may restrict semaglutide or tirzepatide for obesity treatment.

A review published in PubMed Central explains why employer-sponsored plans may restrict coverage of GLP-1 obesity medications. It also discusses access concerns when coverage is removed.

Employers may also use prior authorization, diagnosis rules, or formulary limits. These rules help plans decide who qualifies under the prescription benefit.

This is why employees should first check the exact wording of the plan. HR may need the plan document before reviewing any 2026 coverage request.

How to Check If Your Employer's 2026 Plan Covers GLP-1 Drugs

Start with your employer’s 2026 Summary of Benefits and Coverage. This document usually shows covered benefits, limits, exceptions, and cost-sharing details.

Next, open the plan’s prescription drug list or formulary. Search each medication name separately, not only “GLP-1.”

Check Wegovy, Ozempic, Mounjaro, Zepbound, Rybelsus, and Saxenda. Coverage may differ by diagnosis, plan type, or prescription purpose.

Also look for prior authorization, step therapy, quantity limits, or formulary exclusions. These rules can decide whether the plan covers the drug.

If anything is unclear, ask HR for written benefit details. You can also contact the insurer or pharmacy benefit manager directly. Once you confirm the coverage issue, prepare a simple file before contacting HR.

What to Prepare Before Asking HR About GLP-1 Coverage

Before contacting HR, collect documents that support your coverage request. A clear file can make the discussion more practical and organized.

| Documents or Details | Why It Helps Your HR Request |

|---|---|

| Current plan document | Shows whether GLP-1 drugs are excluded or restricted. |

| Formulary page | Confirms if the drug appears under pharmacy benefits. |

| Denial letter | Explains the exact reason coverage was denied. |

| Prior authorization details | Shows what the insurer requested before approval. |

| Doctor’s support letter | Helps explain medical necessity and the purpose of treatment. |

| Prescription details | Confirms the medication name and prescribed use. |

| Out-of-pocket cost estimate | Shows the financial impact on the employee. |

| Open enrollment deadline | Helps HR understand the timing of the request. |

← Swipe to see more →

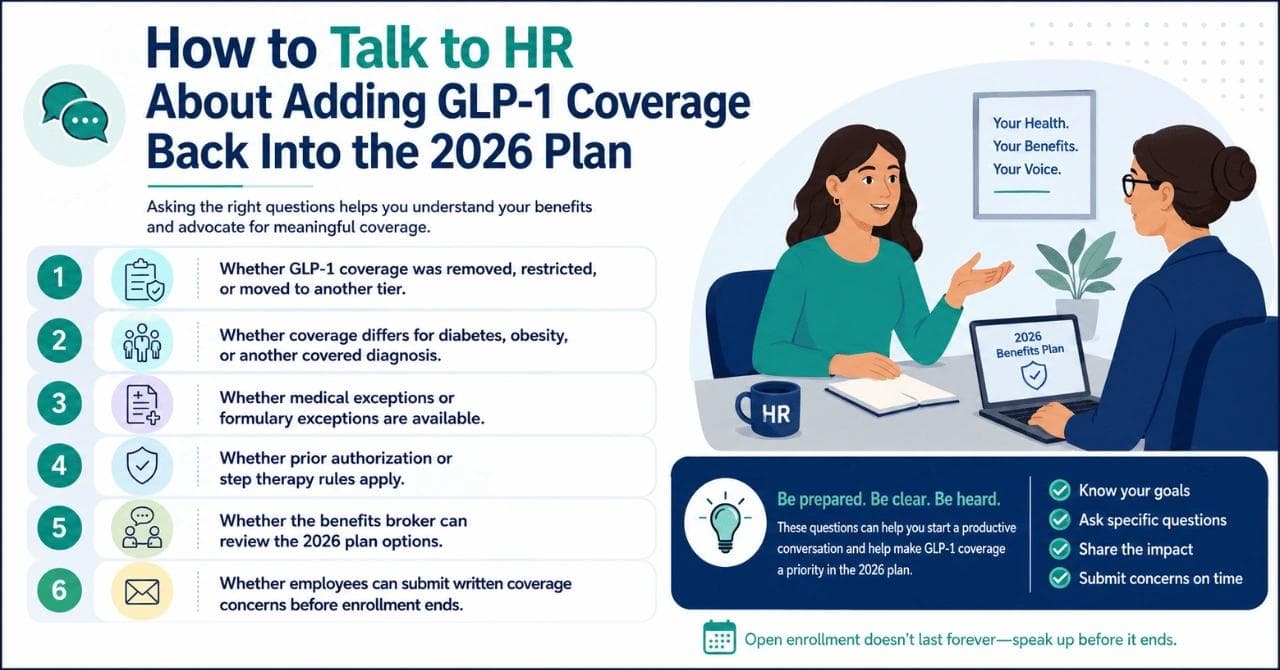

How to Talk to HR About Adding GLP-1 Coverage Back Into the 2026 Plan

Approach HR with a clear request, not an emotional complaint. Keep the discussion focused on plan access, documentation, and next steps. These talking points support employee benefits GLP-1 advocacy without making unsupported claims.

- Whether GLP-1 coverage was removed, restricted, or moved to another tier.

- Whether coverage differs for diabetes, obesity, or another covered diagnosis.

- Whether medical exceptions or formulary exceptions are available.

- Whether prior authorization or step therapy rules apply.

- Whether the benefits broker can review the 2026 plan options.

- Whether employees can submit written coverage concerns before enrollment ends.

Request a written response when possible. This helps your doctor, insurer, and HR stay aligned.

Cost-Benefit Points to Use When Negotiating GLP-1 Coverage With HR

HR teams often review benefits based on cost, access, and employee needs. Your request should reflect that balance.

Explain how sudden coverage loss can affect prescription access. Avoid claiming savings unless you have verified plan data.

A review of GLP-1 obesity medication coverage discusses employer cost and access concerns. This can support strategies for GLP-1 formulary inclusion.

You can also explain why predictable pharmacy benefits matter. Employees may need time to plan appeals, exceptions, or alternative coverage options.

Keep the message professional and document-based. HR is more likely to review a clear request than a general complaint.

Sample Letter to Negotiate GLP-1 Coverage Back Into Your Employer’s 2026 Plan

A written request helps HR understand the issue clearly. Keep the letter short, factual, and document-based.

Subject: Request to Review GLP-1 Coverage for the 2026 Plan

Dear HR Benefits Team,

I am writing to request a review of GLP-1 coverage for the 2026 plan year. My current plan documents show that coverage may be limited, excluded, or unclear.

I would like to understand whether coverage review options are available. Please also confirm if medical exceptions or formulary exceptions can be requested.

I can provide supporting documents if needed. These may include plan pages, denial details, prescription information, and prescriber support.

Could this request be reviewed with the insurer, PBM, or benefits broker? I would also appreciate written guidance on any next steps or deadlines

Thank you for your time and support.

Sincerely,

[Employee Name]

What to Do If Your Employer Does Not Add GLP-1 Coverage Back in 2026

If coverage is not added back, ask for the reason in writing. This can help you understand the next step. You can also ask about appealing GLP-1 insurance denial decisions. Some plans may allow internal appeals or external review.

Review your Summary Plan Description and claims procedure carefully. These documents usually explain deadlines, forms, and required evidence.

Next, compare other legitimate options. These may include ACA Marketplace plans, manufacturer programs, assistance resources, or advocacy organizations.

While you wait for HR or insurer decisions, you may also compare prices at Canadian pharmacies. Polar Bear Meds lists USD pricing for eligible US patients with a valid prescription.

Before ordering, confirm prescription, shipping, import, and pharmacy requirements. Use official sources and current plan documents before making decisions.

Bottom Line: Negotiating GLP-1 Coverage Back Into Your Employer’s 2026 Plan

Negotiating GLP-1 coverage begins with preparation and clear communication. Review your plan documents, gather support, and ask HR specific questions about coverage. Your request should focus on access, plan design, and prescription affordability. Avoid making claims without written plan details.

If coverage is delayed, review appeals, exceptions, marketplace plans, and pharmacy pricing. During the review period, Polar Bear Meds can help you compare prices in USD. Always confirm prescription, shipping, import, and plan rules before ordering.

Frequently Asked Questions

Yes, employer health plans may set their own prescription benefit rules. Coverage can depend on plan design, diagnosis, formulary placement, and exclusions. Employees should check the plan documents before assuming coverage is available.

Coverage decisions may involve the employer, insurer, pharmacy benefit manager, and benefits broker. HR can usually explain who manages the prescription drug benefit. Employees can ask which party reviews formulary changes or coverage concerns.

Yes, open enrollment is a useful time to ask benefit questions. Employees can request written details before choosing a 2026 plan. If coverage is unclear, ask HR about deadlines, exceptions, and plan alternatives.

Share only the information needed for the coverage request. Your doctor or insurer can guide medical-necessity documents when required. Avoid sharing private health details unless they are needed for the review.

Disclaimer

This article is for general information and insurance-navigation purposes only. It is not medical, legal, pharmacy, tax, or insurance advice. GLP-1 coverage can vary by employer plan, diagnosis, formulary, prior authorization rules, exclusions, and prescription purpose. Patients should confirm current coverage, costs, appeals, import rules, and pharmacy requirements with their insurer, HR benefits team, prescriber, pharmacist, and official plan documents before making decisions.