Your Employer Dropped Wegovy or Zepbound Coverage on Jan 1, 2026? Your 7-Day Rescue Plan

If your Employer Dropped Wegovy or Zepbound Coverage on Jan. 1, 2026, act quickly. Many patients search “employer dropped Wegovy January 2026” after a sudden denial. Others describe it as lost Wegovy coverage new year confusion. Confirm the denial reason with your insurer or HR team. Then ask your prescriber about appeal documents or exception requests. This 7-day rescue plan explains how to organize the first week.

How to Confirm If Your Wegovy or Zepbound Coverage Was Dropped by Your Employer

Start by checking your 2026 prescription drug list. Log in to your insurer or pharmacy benefit portal. Search for Wegovy and Zepbound by name. Look for terms like “covered,” “not covered,” “non-formulary,” “plan exclusion,” or “prior authorization required.” Your pharmacy benefits manager (PBM) portal may show the latest drug status. A Plan exclusion is different from a prior authorization requirement.

Next, review your Summary Plan Description or benefits documents. Some employer plans include specific language about weight-loss drug coverage. If the drug is excluded, the issue is different from a prior authorization denial. A denial may still allow an appeal. A plan exclusion usually means the employer plan does not cover that drug category.

Call the pharmacy benefits number on your insurance card. Ask the representative to confirm the current 2026 status. Use clear questions, such as: “Is Wegovy covered under my plan?” “Is Zepbound covered under my plan?” “Is this a plan exclusion or prior authorization issue?” Also ask for the denial reason in writing.

Contact HR to ask if coverage changed during the benefits enrollment lifecycle. Request the latest formulary, Summary Plan Description, and appeal instructions. Keep copies of every notice, portal screenshot, denial letter, and call reference number.

Manufacturer coverage tools can also help you check possible access routes. Wegovy’s official site includes a coverage lookup option. Zepbound’s official site also lists coverage and savings resources. However, always confirm final coverage directly with your insurer or employer plan.

What to Do in the First 24 Hours After Wegovy or Zepbound Coverage Is Dropped

If Wegovy or Zepbound coverage is dropped, focus on proof first.

1. Submit the pharmacy claim: Ask the pharmacy to run the prescription claim. Then request the denial reason or claim response.

2. Call your insurer: Use the pharmacy benefits number on your card. Ask: “Is this a plan exclusion or prior authorization issue?”

3. Save written proof: Keep denial letters, portal screenshots, claim notices, and call reference numbers.

4. Contact your prescriber: Ask whether appeal documents, exception forms, or support letters are possible.

5. Check with HR: Ask whether the employer plan year GLP-1 dropped coverage in 2026.

Your 7-Day Rescue Plan After Employer Wegovy or Zepbound Coverage Loss

If your coverage ended suddenly, organize the first week by priority. A Q1 2026 GLP-1 cut can create fast refill problems. Use each day to confirm documents, appeal options, and cost routes.

| Days | What to Do | Why It Matters |

|---|---|---|

| Day 1 | Confirm the denial reason with your insurer. | You need the exact reason before appealing. |

| Day 2 | Ask HR for the 2026 plan document. | Employer plan rules can change by plan year. |

| Day 3 | Request written denial details from the insurer. | Appeals usually need written documentation. |

| Day 4 | Contact your prescriber about appeal support. | They can provide records or exception forms. |

| Day 5 | Check manufacturer support or savings options. | Some patients may qualify for cost help. |

| Day 6 | Compare cash-pay and pharmacy options safely. | This helps estimate realistic out-of-pocket costs. |

| Day 7 | Choose the safest verified access path. | Avoid rushed decisions after coverage loss. |

← Swipe to see more →

This plan helps organize the first week clearly. Always confirm current rules with your insurer, employer, pharmacy, and prescriber.

Can You Appeal If Your Employer Dropped Wegovy or Zepbound Coverage?

You may be able to appeal if Wegovy or Zepbound was denied. A prior authorization denial is different from a full plan exclusion. An Internal administrative appeal is usually the first review step. Some denied claims may later qualify for external review. An External independent review organization may review eligible disputes.

A prior authorization denial usually has a clearer appeal path. Your prescriber can review the denial and submit supporting records. This may include prior authorization forms, treatment history, or a medical necessity letter.

A full employer plan exclusion can be harder to challenge. It may mean the plan does not cover weight-loss medications. In that case, ask HR for written plan language. Also ask whether any exception process or future coverage review exists.

Keep every document in one place. Save denial letters, claim notices, appeal forms, portal screenshots, and call reference numbers. These records can help if you request an internal appeal or benefits review. An appeal does not guarantee approval. Still, it can clarify your options before you compare cash-pay routes.

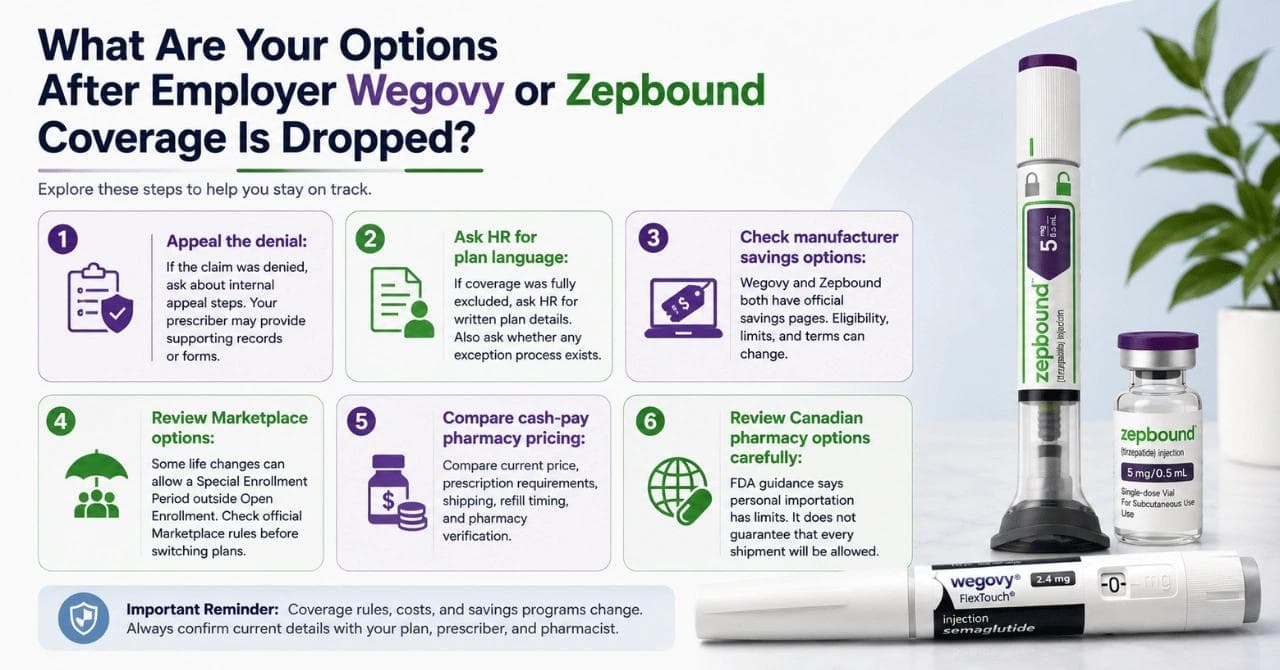

What Are Your Options After Employer Wegovy or Zepbound Coverage Is Dropped?

After employer Wegovy or Zepbound coverage is dropped, review every available route before choosing a cash-pay option. Employer coverage changes can reflect corporate healthcare allocation decisions. That does not always mean every plan follows the same rule.

1. Appeal the denial: If the claim was denied, ask about internal appeal steps. Your prescriber may provide supporting records or forms.

2. Ask HR for plan language: If coverage was fully excluded, ask HR for written plan details. Also ask whether any exception process exists.

3. Check manufacturer savings options: Wegovy and Zepbound both have official savings pages. Eligibility, limits, and terms can change.

4. Review Marketplace options: Some life changes can allow a Special Enrollment Period outside Open Enrollment. Check official Marketplace rules before switching plans.

5. Compare cash-pay pharmacy pricing: Compare current price, prescription requirements, shipping, refill timing, and pharmacy verification.

6. Review Canadian pharmacy options carefully: FDA guidance says personal importation has limits. It does not guarantee that every shipment will be allowed.

How to Compare Wegovy or Zepbound Prices After Employer Coverage Ends

After employer coverage ends, compare prices using the same details each time. Match the same drug, strength, package, and days of supply. Do not compare a starter dose against a maintenance dose. Also avoid comparing one-month pricing with multi-month pricing.

Check manufacturer savings pages first. Wegovy and Zepbound savings programs have eligibility rules, limits, and terms. These offers are not the same as insurance coverage. They can also change without matching your plan year.

Next, review pharmacy cash prices. Check the final checkout price, not only the advertised price. Include prescription requirements, shipping fees, refill timing, and pharmacy verification.

If you compare Canadian pharmacy pricing, use it as one cost route. FDA importation guidance includes limits and case-by-case review. So compare price, prescription rules, shipping, and customs risk together.

Is It Legal to Buy Wegovy or Zepbound From a Canadian Pharmacy After Coverage Loss?

U.S. patients often ask this after employer coverage ends. The safer answer is that importing prescription drugs for personal use is restricted in most cases. FDA guidance says personal importation may be considered only in limited situations.

That means Canadian pharmacy ordering should not be treated like a guaranteed legal shortcut. Patients should check FDA guidance, use a valid prescription, and choose only verified pharmacy sources. Customs review can still affect whether a shipment is allowed. Check the medication name, prescription requirement, quantity, shipping rules, and pharmacy credentials. Also confirm whether the pharmacy explains importation limits clearly.

Final Thoughts on Employer Wegovy or Zepbound Coverage Loss in 2026

Employer Wegovy or Zepbound coverage loss can disrupt refill plans quickly. A Q1 2026 GLP-1 cut shows why patients must verify their own plan rules. Use the 7-day rescue plan to organize documents, appeal routes, and cost comparisons. If Canadian pharmacy pricing is part of your review, Polar Bear Meds is one option to compare Wegovy pricing in USD.

First-time buyers can also check whether the WELCOMEPB10 discount applies at checkout. Before ordering, confirm the current price, prescription rules, shipping details, and FDA importation guidance.

Frequently Asked Questions

Yes, employer health plans can change covered benefits by plan year. Some changes may affect patients already using Wegovy or Zepbound. Always check your current formulary, plan documents, and HR benefits notice before assuming coverage continues.

Not always. Losing drug coverage alone may not qualify as a Special Enrollment Period. However, broader coverage loss or certain life events might qualify. Check official Marketplace rules before changing plans.

Possibly, if the medication is prescribed and the expense meets plan rules. HSA and FSA rules can vary by administrator. Ask your benefits provider before using funds for cash-pay prescriptions, shipping, or pharmacy charges.

Disclaimer

This blog is for general information and cost-comparison purposes only. It is not medical, legal, insurance, pharmacy, or treatment advice. Wegovy and Zepbound pricing, availability, insurance coverage, appeal rules, prescription requirements, shipping timelines, and pharmacy policies can change. They may vary by employer plan, insurer, pharmacy, location, and access route. Always consult your prescriber, insurer, HR benefits team, pharmacist, or official resources before making coverage or purchase decisions.